If you're planning to buy a home in the Huntsville area, one of the first questions that usually comes up is:

“How long does it actually take to buy a home in Huntsville?”

The short answer: Most home purchases in Huntsville, Madison, and Limestone County take about 30–45 days from accepted offer to closing when financing is involved.

National mortgage data consistently shows the same timeline. For example:

• Chase Bank reports an average closing timeline of about 43 days once the mortgage process begins

However, that timeline can change depending on several factors:

• Loan type

• Inspection negotiations

• Appraisal timing

• Title work

• Market conditions

Understanding what happens during those weeks can help you avoid delays, reduce stress, and make better decisions during the purchase process.

At the Rebecca Lowrey Group RE/MAX Distinctive, our team guides buyers through this process every day, including many people relocating to Huntsville for jobs at Redstone Arsenal, Research Park, the FBI, and the region’s expanding aerospace and defense industry.

In this article, we’ll walk through:

• The typical Huntsville home buying timeline

• What happens after your offer is accepted

• How inspections and financing affect closing

• What the Alabama closing process actually looks like

• Practical tips that can help your purchase move faster and more smoothly

The Typical Timeline to Buy a Home in Huntsville

While every real estate transaction is unique, most home purchases follow a similar timeline.

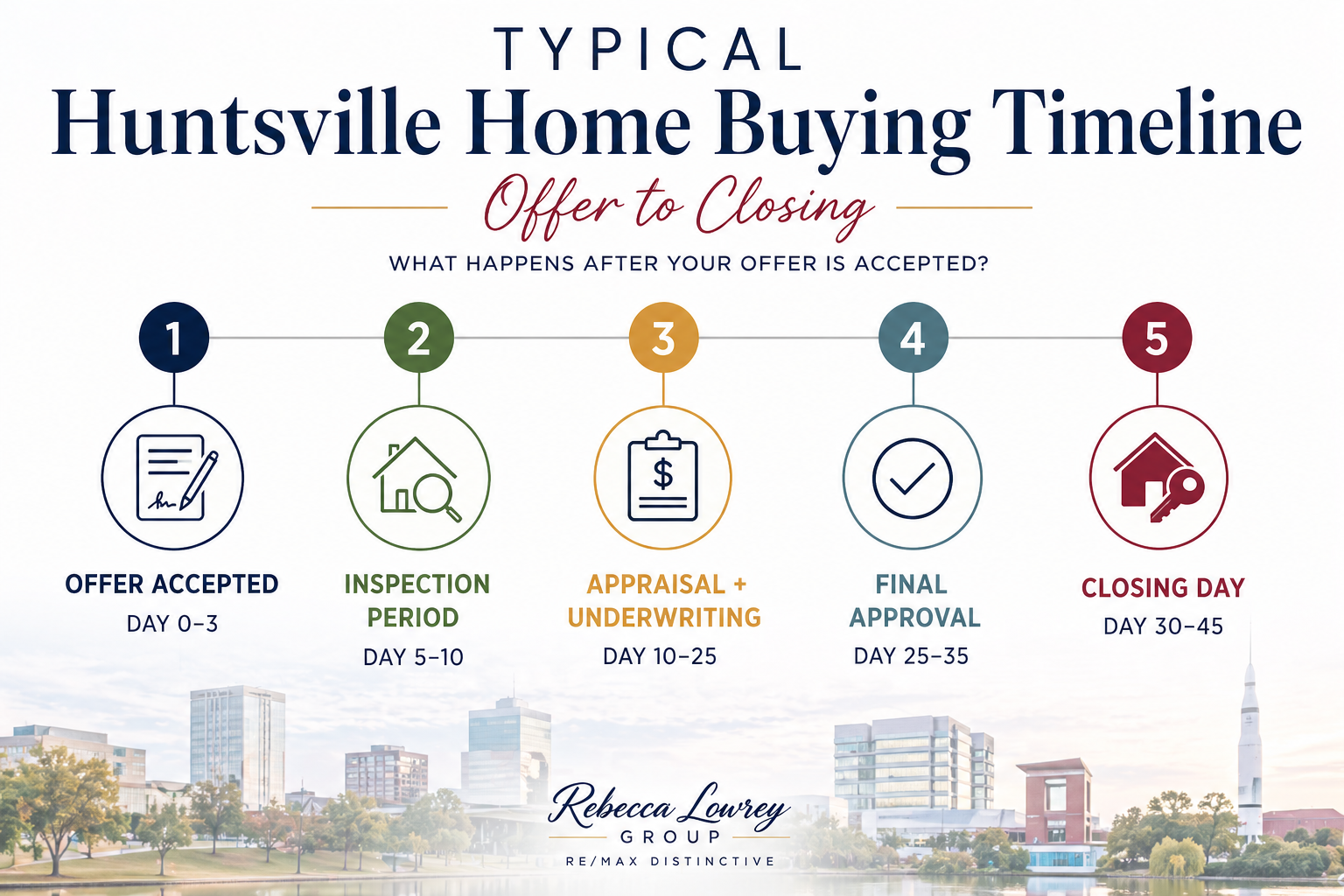

Typical timeline after your offer is accepted:

Day 1–3

Earnest money deposit and scheduling inspections

Day 5–10

Home inspection and repair negotiations

Day 10–25

Appraisal and lender underwriting

Day 25–35

Loan approval and closing preparation

Day 30–45

Final walkthrough and closing

Mortgage-financed purchases generally close within this 30–45 day window, though some transactions may take up to 60 days depending on loan type and complications.

Cash purchases are usually much faster. Often, one to two weeks pass since there is no mortgage underwriting involved.

Important factors that influence your closing timeline

Many buyers assume the lender is the main reason transactions take time.

In reality, several moving parts must align:

• Inspection scheduling

• Appraisal availability

• Title research

• Loan underwriting review

• Repair negotiations

Mortgage underwriting alone can take three to four weeks, depending on documentation and lender workload. This is why experienced real estate teams closely track every step of the transaction.

At the Rebecca Lowrey Group, we coordinate communication between lenders, inspectors, title companies, and agents to help keep everything moving forward on schedule.

Advantages and disadvantages of faster closings

Advantages

• Sellers may prefer quick closings and favor your offer

• You reduce exposure to interest rate changes

• You get possession sooner

Potential drawbacks

• Less time for inspection negotiations

• Increased pressure on lenders and title companies

• Limited flexibility if repairs are discovered

The right timeline balances speed with proper due diligence.

Step 1: Getting Pre-Approved Before Touring Homes

Before most buyers begin touring homes, the first step should always be mortgage pre-approval.

A pre-approval helps determine:

• Your estimated monthly payment

• Maximum purchase price

• Loan type eligibility

• Budget expectations

Pre-approval also signals to sellers that you are financially prepared to purchase the home.

Why does this matter in Huntsville specifically?

Huntsville has seen significant population growth due to jobs in technology, aerospace, and defense. Many buyers relocating here are moving from higher-cost markets. Understanding local financial differences, especially property taxes, is important when planning your budget.

For example, Alabama property taxes are among the lowest in the United States because owner-occupied homes are taxed on only 10% of assessed value. Lower property taxes are one reason many relocating buyers find housing in Huntsville more affordable than in states like California, Illinois, or Texas.

Step 2: Submitting an Offer on a Home

Once you find a home you want to purchase, your real estate agent helps you prepare a purchase offer.

Offers typically include:

• Purchase price

• Earnest money amount

• Financing terms

• Inspection contingency

• Requested closing timeline

Earnest money is a deposit submitted with the offer that shows the seller you intend to complete the purchase. Most earnest money deposits fall within 1% to 3% of the purchase price, though the amount can vary based on market conditions and negotiation.

Real estate professionals also note that many Alabama markets commonly see deposits around 1%–3% or flat amounts like $1,000–$5,000, depending on price point. The deposit is typically held in an escrow account and later applied toward the buyer’s down payment or closing costs if the sale proceeds.

Strategic decisions buyers often overlook

Many buyers assume price is the only factor sellers consider.

But sellers often evaluate the entire structure of the offer, including:

• Strength of financing

• Amount of earnest money

• Closing timeline

• Flexibility of possession date

• Inspection contingencies

In competitive neighborhoods around Huntsville, such as Blossomwood, Five Points, or parts of Madison. These details can influence which offer is accepted.

Step 3: The Home Inspection Period

After the purchase agreement is signed, the inspection phase begins. Inspection windows in many Alabama contracts are typically 7–10 days, giving buyers time to evaluate the home’s condition and negotiate repairs if necessary.

A standard home inspection evaluates:

• Roof condition

• Structural integrity

• Electrical systems

• Plumbing systems

• HVAC performance

• Drainage or moisture issues

Negotiating repairs

If issues are discovered, buyers can typically request:

• Repairs completed before closing

• A price reduction

• Seller credits toward closing costs

Negotiations must occur within the contract’s inspection deadline.

Step 4: Appraisal and Mortgage Approval

During the inspection period, the lender begins the appraisal and underwriting process. The appraisal confirms the property’s market value for the lender. If the appraisal comes in below the purchase price, buyers and sellers may need to renegotiate.

Meanwhile, the lender reviews financial documentation, including:

• W-2 income verification

• bank statements

• credit reports

• debt-to-income ratio calculations

Common mistakes buyers make during this phase

• Opening new credit accounts

• Changing jobs during escrow

• Making large unexplained bank deposits

• Financing new purchases before closing

These actions can delay loan approval or even jeopardize the mortgage.

Step 5: The Closing Process in Huntsville

Closing is the final step where ownership of the home transfers to the buyer.

In the Huntsville area, closings are typically handled by real estate attorneys or title companies.

During closing:

• Loan documents are signed

• Funds are transferred

• Title ownership is recorded

The closing appointment itself usually takes about one hour, assuming documents are prepared, and no issues remain outstanding. Before closing, buyers typically complete a final walkthrough of the property to confirm the home's condition and verify agreed repairs were completed.

Why the Right Real Estate Team Makes the Process Easier

Buying a home involves coordination between many professionals:

• Lenders

• Inspectors

• Appraisers

• Title companies

• Contractors

• Agents

Without strong communication, delays can happen quickly.

The Rebecca Lowrey Group RE/MAX Distinctive helps buyers navigate these moving parts with a structured process and local expertise. For buyers relocating to Huntsville, especially those moving for jobs at Redstone Arsenal, Research Park, or the FBI, having experienced local guidance can make the entire process significantly smoother.

Frequently Asked Questions

How long does it take to buy a home in Huntsville?

Can you close faster than 30 days?

Yes. Cash purchases may close in one to two weeks since no mortgage underwriting is required.

How much earnest money is typical in Alabama?

What happens if inspection issues are discovered?

Buyers can negotiate repairs, request seller credits, or, in some cases, cancel the contract if contingencies allow.

The Bottom Line

Buying a home in Huntsville typically takes about 30–45 days once your offer is accepted, but the timeline depends on inspections, financing, and negotiations.

Understanding each step of the process helps buyers move through the transaction with confidence.

From inspections and appraisals to underwriting and closing day, having the right guidance ensures every stage stays on track.

For buyers relocating to the Huntsville area or purchasing locally for the first time, the Rebecca Lowrey Group RE/MAX Distinctive helps simplify the process with local expertise, clear communication, and strategic guidance.

Amanda Holifield | Rebecca Lowrey Group | RE/MAX Distinctive

Top 1% Nationally | 345+ Five-Star Reviews

Huntsville, Madison & North Alabama Real Estate Specialists

Information is current as of April 2026 and is provided for general informational purposes only. Timelines referenced in this article, including the typical 30–45 day closing period, may vary based on financing type, market conditions, inspection outcomes, title work, and lender requirements. Alabama follows “buyer beware” principles in many resale transactions, meaning buyers are responsible for conducting their own due diligence on property condition. This content is not intended as legal, financial, or tax advice. Rebecca Lowrey Group does not guarantee timelines, property condition, or third-party vendor performance. Buyers should complete all inspections and consult with licensed professionals, including lenders, inspectors, and closing attorneys, before making a purchase decision.